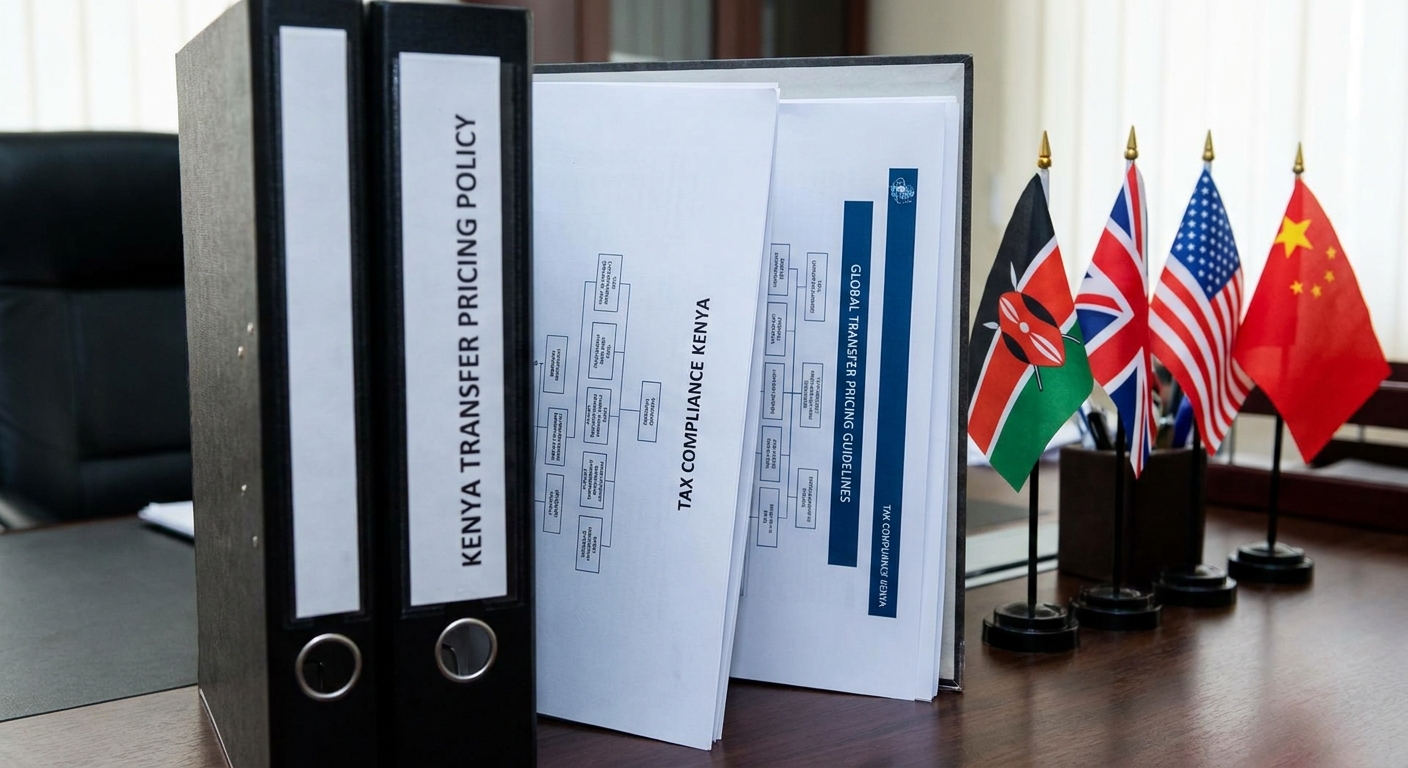

Transfer pricing is one of the most complex areas of tax compliance, yet it affects a wide range of businesses in Kenya — including family groups, companies with overseas affiliates, and businesses that share common ownership.

What is Transfer Pricing?

Transfer pricing refers to the prices set for transactions between related parties — such as a parent company selling goods to a subsidiary, or a director lending money to their company. KRA requires these transactions to be priced at "arm's length" — i.e., as if the parties were independent.

Kenya's Rules

The Income Tax Act and KRA guidelines require:

- Documentation of all related-party transactions

- Evidence that prices reflect arm's length values

- Master file and local file documentation for businesses above KSh 500 million annual turnover

- Country-by-country reporting for multinationals above EUR 750 million global turnover

Common Related-Party Transactions

- Management fees between parent and subsidiary

- Interest on inter-company loans

- Royalties for use of intellectual property

- Shared service costs

Our tax advisors help businesses document related-party transactions correctly, prepare transfer pricing policies, and ensure full compliance with KRA guidelines — avoiding costly adjustments and penalties.